Bull Market Cycle: Climbing the Wall of Worry

- Chris Harris, CFP® , FMVA

- Apr 27

- 5 min read

It has now been over three-and-a-half years since the current bull market got underway in October 2022. At that time, inflation was surging at its fastest pace in fifty years, the Fed was aggressively raising interest rates, and ChatGPT had yet to be released to the public. Since then, the S&P 500 has more than doubled in value and the Bloomberg U.S. Aggregate Bond index has fully recovered.

While the world looks quite different today, market concerns continuing to make headlines is nothing new. Every cycle brings fresh challenges and raises questions about whether the fundamental rules of investing remain applicable. The reality is that each cycle is unique, with its own catalysts, innovations, and sources of uncertainty. And yet, the core principles of investing and financial planning have remained consistent across decades, continuing to guide investors in the right direction.

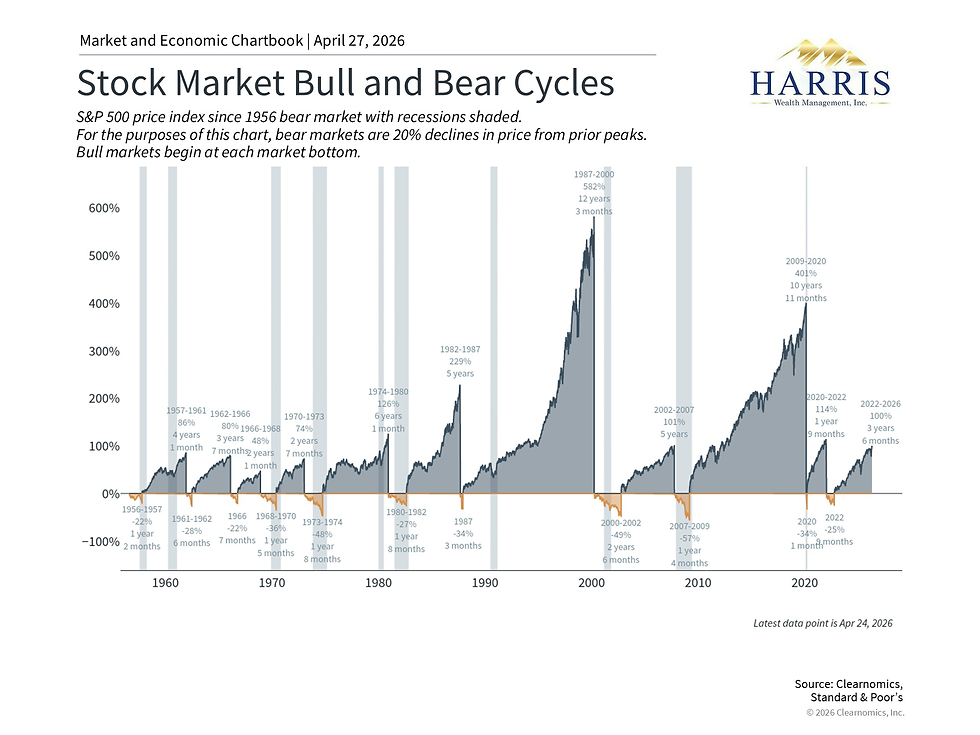

Bull markets consistently climb a wall of worry

Although geopolitical developments continue to influence markets, the broader market cycle may be the more meaningful consideration for long-term investors. With the market hovering near all-time highs, it is natural for some investors to be concerned about pullbacks and corrections. These events occur with some regularity, historically, the S&P 500 has experienced four or five pullbacks of 5% or worse in a given year, on average.1

While such events are never comfortable, long-term investing is shaped much more by historical patterns spanning years and decades. This is one reason why overreacting to short-term market movements can be counterproductive, potentially leaving investors poorly positioned relative to their long-term financial goals.

It is often said that the market climbs a "wall of worry" over time. In recent years, markets have navigated high inflation, a banking crisis in 2023, geopolitical conflicts, concerns about a Fed policy misstep, AI-driven market concentration, tariff-related volatility, and more. None of these challenges were insignificant, and yet markets have continued to perform well throughout.

The chart above illustrates this pattern going back to World War II. Over this 70-year span, bull markets have lasted considerably longer and produced much larger gains than what is lost during bear markets. Bear markets have typically lasted one to two years on average, whereas recent bull markets have extended as long as ten years or more. Even when corrections occur within bull markets, the average decline is 14%, with the average recovery taking just four months.2

Consider the bull market that followed the 2008 financial crisis, which lasted nearly eleven years. Despite this impressive run, it is often described as "the most unloved bull market" because there was a persistent stream of market and economic concerns throughout. In hindsight, it is clear that even when those concerns were legitimate, such as questions about the pace of economic recovery or the trajectory of the national debt, they did not justify making changes to long-term portfolios.

Of course, past performance is no guarantee of future results, and the speed of any market recovery depends on the circumstances at hand. However, the historical record consistently demonstrates that attempting to react to every market movement has, more often than not, caused investors to miss a significant portion of the subsequent gains.

A healthy economy underpins long-term market returns

Although the stock market and the broader economy are distinct, they are closely connected. Corporate earnings, which ultimately depend on economic growth, are the primary driver of stock prices over the long run. This is why monitoring the broader economic cycle matters, even as markets react to a variety of factors on a day-to-day basis.

The current business cycle has technically been running two-and-a-half years longer than the current market cycle. The most recent official recession, as determined by the National Bureau of Economic Research, was the brief but sharp contraction triggered by the pandemic in 2020. Since then, there have been periods of slower growth and occasional recession forecasts, none of which have materialized.

By many measures, the economy remains in good health today, though there are three key areas that investors are monitoring closely. First, oil prices above $100 per barrel, if sustained, could weigh on consumer spending and contribute to inflationary pressures. Second, the labor market has slowed noticeably, particularly in areas such as technology, raising questions about the durability of consumer spending, which has been a key driver of growth in recent years. Third, the scale of AI-related investments has prompted debate about whether a "bubble" is forming, an understandable concern for investors who have lived through both the dot-com bust and the housing crisis.

Identifying bubbles in real time is notoriously difficult, and history shows that periods of elevated valuations do not always end in dramatic collapses. So far in this cycle, earnings growth has supported valuations and many companies are funding significant investments from their own profits, unlike in past cycles. For long-term investors, maintaining a balanced exposure across different parts of the market remains the key to participating in growth while managing risk.

Stocks and bonds continue to complement each other

Every market cycle tends to raise questions about whether traditional portfolio management principles remain valid. In 2022, when both stocks and bonds declined simultaneously in response to rapidly rising inflation and interest rates, some investors questioned whether bonds still played a meaningful role in a diversified portfolio. Similar doubts emerged after the 2008 financial crisis, when historically low interest rates weighed on bond performance.

Over the past few years, bonds have not only recovered but also provide meaningful income and portfolio stability. The Bloomberg U.S. Aggregate Bond Index has posted positive returns in each of the past two years, helping to cushion periods of equity market volatility. International stocks and commodities have also contributed, offering additional diversification benefits.

This experience aligns with what history demonstrates across cycles. Every era seems to prompt the question of whether "this time is different" with respect to the relationship between asset classes. In the 1970s, inflation tested traditional portfolios. During the dot-com era, technology stocks became enormously popular despite limited corporate profits, making other sectors seem unappealing by comparison. In 2022, rising rates placed simultaneous pressure on both stocks and bonds. Echoes of each of these challenges can be found in today’s environment.

Each time, a commitment to diversification and long-term investing has proven to be the right course of action. As uncertainty persists and new headlines continue to drive market swings, maintaining focus on the broader picture is more important than ever.

Please feel free to reach out with any questions!

Footnotes

1. The number of pullbacks is based on S&P 500 index price returns since 1980.

2. The average size of corrections and recovery time are calculated from S&P 500 index total returns, since World War II.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Examples are for illustrative purposes only. All investing involves risk of loss including the possible loss of all amounts invested.

Comments