What Q1 2026 Teaches Us About Investing Through Uncertainty

- Chris Harris, CFP® , FMVA

- Apr 2

- 7 min read

What a wild first quarter! The first three months of 2026 offer a valuable lesson in why preparation matters in financial planning and investing. Following solid gains in 2025, markets were rattled by a mix of global tensions, rising oil prices, and fresh economic worries. A conflict in Iran, which broke out at the end of February, became the biggest market story of the quarter. It pushed oil prices sharply higher and triggered the first notable market decline of the year. By the end of March, though, reports of a possible ceasefire began to surface, and the situation is still developing.

Stepping back for a wider view, markets have still delivered strong results over the past twelve months overall. Several parts of the market — including energy stocks and more stable, “defensive” sectors — helped support portfolios during the turbulence. Looking ahead, new questions will likely emerge in the coming months, including a leadership change at the Federal Reserve (the U.S. central bank) and midterm elections later in the year.

For investors with long-term goals, the first quarter is a helpful reminder that markets rarely go up in a straight line, and that the foundations of good investing matter most when things feel uncertain.

Key Market and Economic Highlights

• The S&P 500 (a broad measure of large U.S. company stocks) had a total return of -4.3% in Q1, the Nasdaq (technology-heavy index) returned -7.0%, and the Dow Jones Industrial Average returned -3.2%.

• The Bloomberg U.S. Aggregate Bond Index (a broad measure of U.S. bonds) was roughly flat for the first quarter of 2026. The 10-year Treasury yield — a key interest rate benchmark — ended the quarter at 4.3% after falling as low as 3.9% at the end of February.

• Stocks in developed international markets (MSCI EAFE) fell -1.1% and stocks in emerging markets (MSCI EM) declined -0.1% over the quarter, both measured in U.S. dollar terms.

• Oil prices surged, with Brent crude reaching $118 per barrel at the end of March after starting the year under $61. WTI (another oil benchmark) ended the quarter at $101 per barrel.

• Gold ended the quarter at $4,668 per ounce after climbing as high as $5,417 in January. The U.S. Dollar Index (DXY), which measures the dollar against other currencies, strengthened slightly to 99.96.

• February inflation data showed the headline Consumer Price Index (CPI) rising 2.4% compared to a year earlier, while core CPI (which excludes food and energy) rose 2.5%. The core PCE price index — the Federal Reserve’s preferred inflation measure — rose 3.1% year-over-year in January.

• The Federal Reserve kept its benchmark interest rate unchanged in a range of 3.50% to 3.75% at both of its meetings during the first quarter.

The first market pullback of the year arrived in Q1

It is easy to notice similarities between the start of this year and the beginning of 2025, as both were shaped by global concerns. Interestingly, both first quarters saw the S&P 500 decline by the same amount: 4.3%. Last year’s turbulence was driven by tariffs, while this year’s was caused by the conflict in the Middle East. Even so, the effect on how investors felt was similar in both cases. When uncertainty rises, markets often react sharply to news headlines in the short term.

History does not guarantee future results, but looking back can help us understand how markets have typically behaved. Despite the difficult first quarter of 2025, stocks went on to post strong gains for the rest of that year, including dozens of record highs across major indexes. The key point is not that markets always bounce back quickly, but that market conversations tend to focus heavily on bad news. When recoveries do happen, they often catch investors by surprise.

Perhaps the most useful thing to remember is that market pullbacks — periods when prices drop from recent highs — are a normal and unavoidable part of investing. Since 1980, the S&P 500 has seen an average mid-year decline of around 15%, even though markets tend to finish with positive returns in more than two-thirds of all years. In a typical year, investors can expect four or five drops of five percent or more. Last year saw six such pullbacks, yet the S&P 500 still finished with an 18% total return.

The main takeaway for investors is that short-term swings — especially those driven by news headlines — are simply part of the normal market cycle. Portfolios built around long-term financial goals are specifically designed to navigate these periods. This is especially worth keeping in mind as the midterm election approaches and concerns about government spending may resurface later in the year.

Geopolitics and energy prices are the biggest sources of uncertainty right now

The most significant market event of the first quarter was the escalating conflict in the Middle East, which sent oil prices higher. Disruptions to the Strait of Hormuz — a critical waterway that carries roughly 20% of global oil from the Persian Gulf to the rest of the world — led major oil-producing countries in the region to cut production. Brent crude ended the quarter at $118 per barrel, up over 94% since the start of the year. WTI crude also surpassed $100, the highest level since the war in Ukraine began in 2022. Oil prices will likely continue to respond to developments in the region, including any news around a possible ceasefire.

Higher energy costs hit consumers directly at the gas pump and also push up prices for goods and services more broadly throughout the economy. The average price of gasoline across the country reached $4 per gallon at the end of March, and diesel prices have jumped sharply as well.

While these developments do affect household budgets, economists tend to view these kinds of “supply-side shocks” — sudden price increases caused by disruptions to supply rather than changes in demand — as temporary. That is because oil prices typically recover once the underlying geopolitical event stabilizes. This was the pattern in 2022, when gas prices hit $5 before falling within months. While higher prices are certainly uncomfortable, the current gasoline levels are not expected to cause serious financial hardship for the average American household.

History also shows that geopolitical events, while unsettling in the short term, have rarely derailed markets over the long run. This includes the U.S. operation in Venezuela in January, which caught markets off guard but had little lasting impact on investments. While the current conflict is still evolving and the human cost is significant, investors who made dramatic changes to their portfolios in response to past crises often did so at the wrong time.

The economy is slowing down but remains healthy overall

Rising energy prices are just one part of the larger economic picture. Other signals suggest the economy has cooled over the past year but remains fundamentally sound — this comes after several years during which many investors and economists predicted recessions that never arrived.

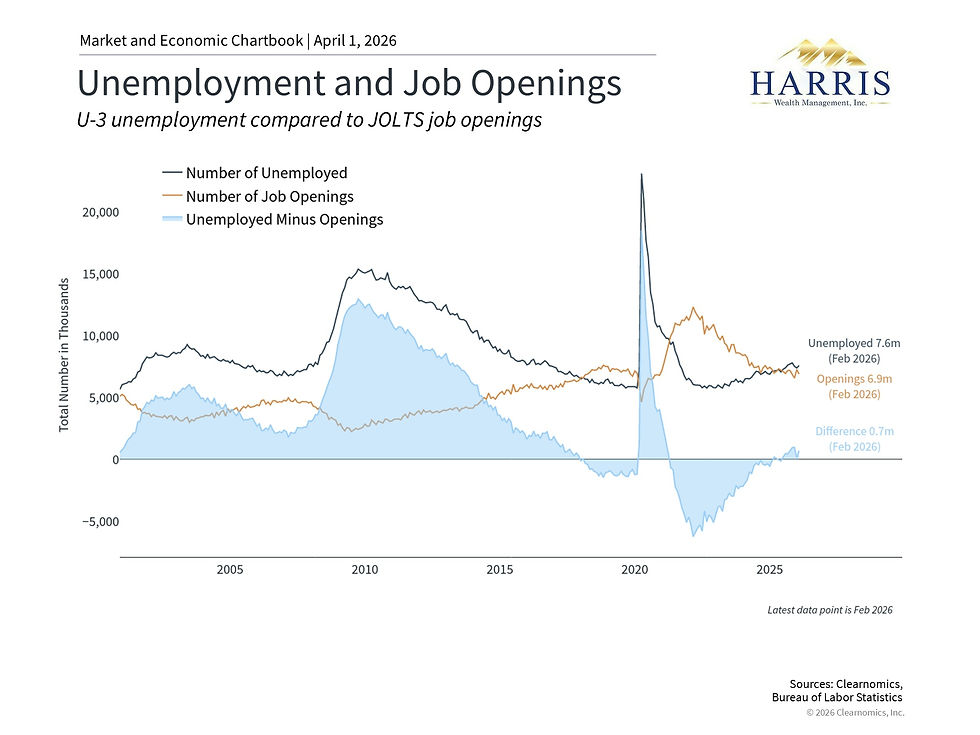

One of the most closely watched areas is the job market. The latest data show that job gains fell by 92,000 in February and the unemployment rate edged up to 4.4%. Notably, the number of people looking for work now exceeds the number of available job openings for the first time in years. As recently as 2022, there were two job openings for every unemployed person — an unusually tight labor market. That balance has now shifted.

Context is important here, though. Fewer people are entering the workforce due to lower immigration levels and an aging population. In other words, both the supply of workers and the demand for workers are cooling at the same time, which has helped keep the unemployment rate near historically low levels. Investors pay close attention to jobs data because employment directly affects household income, consumer confidence, and spending. Consumer spending accounts for more than two-thirds of U.S. economic output (GDP), and it has remained stronger than many expected over the past several quarters.

Different parts of the market have moved in very different directions

While the overall S&P 500 has declined this year, results across different market sectors — groups of companies in similar industries — have varied widely. In fact, six of the eleven S&P 500 sectors are still positive for the year, and the gap between the best and worst performing sectors grew to nearly 50 percentage points during the first quarter.

The Energy sector has been the standout leader, gaining nearly 40% through the end of March, as higher oil prices are expected to boost company revenues and attract further investment. Other sectors posting gains include Consumer Staples (everyday household goods), Utilities, Materials, and Industrials, all of which have benefited from a more cautious market environment. These are often called “defensive” sectors because they tend to include more stable businesses with steadier earnings that are less sensitive to economic ups and downs.

On the other hand, the Information Technology sector has declined approximately 9%, and many of the large technology companies that make up the Magnificent 7 have underperformed. This marks a shift from recent years, when a small group of large tech companies drove the majority of overall market gains.

As always, it is important to keep these moves in perspective. As the chart above illustrates, sector leadership can shift depending on market and economic conditions. Energy was the top-performing sector in 2021 and 2022, when technology stocks struggled. That then reversed over the following three years. Just as with different asset classes, it is very difficult to predict which sector will lead or lag in any given year — which is why a well-diversified portfolio is better positioned to handle a variety of market environments.

The tariff landscape continues to shift

Trade policy also took a significant turn at the end of January, when the Supreme Court ruled 6-3 that the broad tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were unlawful. In response, the administration put in place a temporary global import duty under a different law — Section 122 of the Trade Act of 1974. The administration also launched new Section 301 trade investigations in March, while roughly a dozen Section 232 investigations are still ongoing.

For investors, the key point is that while the legal basis for tariffs has changed, the broader direction of trade policy is likely to continue. Tariffs will probably keep affecting the economy through consumer prices, business costs, and investor confidence. That said, last year demonstrated that markets can adapt to these kinds of policy changes over time. So, regardless of how the tariff situation unfolds later this year, the important thing is to stay invested and avoid overreacting to policy headlines.

Comments