The Two-Faced Consumer: Why Americans Feel Poor but Keep Spending

- Chris Harris, CFP® , FMVA

- 2 days ago

- 5 min read

Consumer spending drives the U.S. economy, making up about two-thirds of all economic activity. When people feel financially secure, they tend to spend more, which helps businesses earn more and supports overall economic growth. When people feel worried, they may cut back. In practice, spending behavior depends on many factors, and not all households are in the same situation. That is why getting a full picture of how consumers are doing financially is one of the most useful things a long-term investor can do to understand what is happening in the economy today.

Right now, that picture is positive but complicated. On the positive side, household net worth (the total value of what people own minus what they owe) is close to record levels, the job market has gotten better, retail sales are strong, and gasoline prices are coming down. On the more cautious side, consumer sentiment (how people feel about their finances and the economy) is near historic lows, savings rates have dropped, debt levels are high, and inflation (rising prices) is still above the Federal Reserve's target.

These mixed signals point to an economy that is generally doing well, but one where some households still feel stretched. For long-term investors, understanding both the strengths and the pressures in consumer finances helps make sense of economic trends and underscores why following a sound financial plan matters.

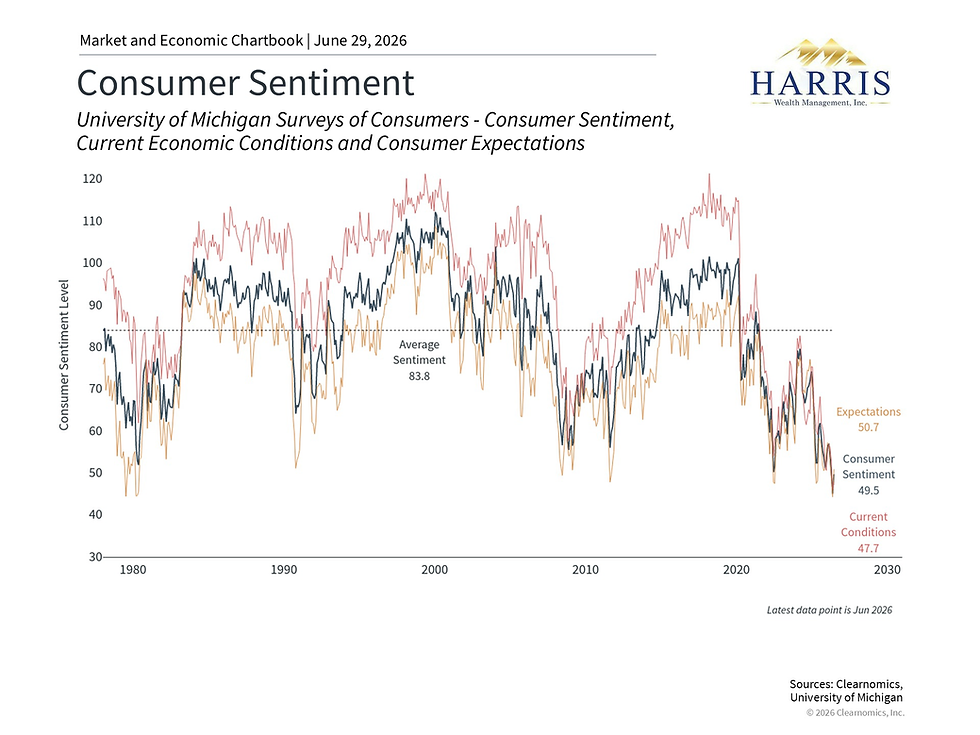

Consumers feel pessimistic even as spending stays strong

The University of Michigan Surveys of Consumers measures how people feel about their financial situation and the broader economy. In June 2026, that index came in at 49.5, far below the historical average of 83.8. This puts consumer sentiment close to its all-time low, similar to levels seen during the 2008 financial crisis and the early days of the pandemic. The same survey showed that people expect prices to be 4.6% higher one year from now, suggesting that concerns about inflation are a key reason for the negativity.1

You might expect that when people feel bad about their finances, they would stop spending. But that is not always how it works. Sentiment surveys measure what people say, not necessarily what they do. In fact, retail sales (the total amount spent at stores and online) grew 6.9% compared to the same period last year, well above the long-term average of 4.7%.2

What explains this gap between how people feel and how they spend? A big part of the answer is the lasting impact of inflation over the past several years. Even though the rate of price increases has slowed, everyday items like groceries, housing, and energy still cost much more than they did before the pandemic. People may feel pessimistic in surveys because of those higher prices, even while they continue spending on things they need and some things they want.

The job market has been improving, but there is still some uncertainty, including concerns about how artificial intelligence may affect employment in the future. Wage growth (how fast pay is rising) has slowed to an annual rate of 3.6%, which is still historically strong, but it is below recent inflation readings driven by energy prices. These wide-ranging concerns may shape how households feel about the future, even if they keep making purchases.

Household net worth reflects the underlying strength of the economy and markets

Even though consumer sentiment is low, the overall financial position of American households has never been stronger. Total U.S. household net worth reached $183 trillion in the first quarter of 2026, a record high. Financial assets such as stocks and retirement accounts have grown significantly during the current market cycle. The value of non-financial assets like homes has also risen over the past several years.3

Of course, this broad picture does not apply equally to everyone. A popular way to describe this is a "K-shaped" economy, where households that own financial assets or real estate have seen their wealth grow considerably. For those without such assets, wages have grown strongly, but many are also carrying higher levels of debt. Across the country, credit card debt has climbed to $1.3 trillion, auto loans to $1.7 trillion, and student loan balances to $1.7 trillion.4

The "wealth effect" helps explain why overall spending has stayed resilient even as sentiment has fallen. This is the tendency for people to spend more when they feel wealthier, for example because their home value or investment account has gone up. For the health of the broader economy, it is better when financial growth is spread across many segments of the population. For investors focused on markets and portfolios, what matters most is the growth rate of corporate earnings. So while some households may be facing challenges, this does not automatically translate into a concern for investors.

Savings rates have dropped to historically low levels

The personal savings rate measures how much of their after-tax income people save rather than spend. Today that rate stands at just 3.0%, well below the historical average of 6.2%. For much of the twentieth century, Americans saved far more, averaging 11.1% between 1960 and 1990. The current rate is also a sharp reversal from the pandemic period, when savings briefly spiked above 30% as government support came in and there were fewer opportunities to spend.5

Several factors explain why savings have fallen. Strong consumer spending means more money is being spent than saved. Higher prices for necessities like gasoline also leave less of each paycheck available to set aside. There is also a demographic factor: as the Baby Boomer generation moves further into retirement, they are drawing down the savings they built up over their working lives, which naturally brings down the overall savings rate. These long-term population shifts help explain why the rate has trended lower over recent decades.

A savings rate of just 3.0% can leave households with little cushion for unexpected expenses or major life events. From a financial planning standpoint, this is an important area to pay attention to. For long-term investors, the power of compounding (earning returns on top of returns over time) means that money saved early in a financial plan can grow significantly over decades.

Looking at the broader picture, there are encouraging signs as well. Oil prices have come down from recent highs, which could help ease inflation and reduce some of the pressure that has been weighing on how consumers feel. The job market has shown improvement in hiring activity, and unemployment remains low. These are positive developments for households and for the overall outlook for consumer finances.

Have a wonderful and safe summer!

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Examples are for illustrative purposes only. All investing involves risk of loss including the possible loss of all amounts invested.

Comments